On April 24, 2019, NIC released a study that explored the senior living needs of middle-income aging Boomers.

By Steve Moran

The leadership at NIC has for a year been talking about a study they commissioned to explore the senior living needs of middle-income aging Boomers. On April 24, 2019, the study was released at a big event in Washington, D.C. This is a longer than typical article that will start with some report highlights, followed by my assessments of what is missing, and why those missing pieces could be important. This article will close with an analysis of what it means and where I see opportunities.

This article is based on the report itself, the roll-out presentation, other resources on the NIC Middle Market microsite — and a long and helpful conversation with Beth Mace, NIC’s head economist.

A caveat: the “what’s missing” part of this article is not intended to be a criticism. Most, if not all, of the things I talk about in that section, were considered by those involved in the study. It is impossible to study everything and to explore every nook and cranny of the universe of anything . . . in this case Senior Living.

You can download the study HERE.

Preamble – I am Optimistic

During my first pass through the press release — and even listening to the webcast about the report — it was pretty easy to see a half-empty glass — or more precisely, a 54% empty glass. And, for sure, this is a problem that could turn into a crisis; however, I am super optimistic that it will be solved along the way in four broad ways:

-

The industry will figure out new ways to serve this population.

-

There will be more flexibility that allows government dollars to be used to pay a portion of costs.

-

Regulations will flex — allowing for more creative solutions like volunteer workers, “pay it forward” credit banking, and inter-generational living that includes assisted living.

-

There will be advances in creative programming that might include technology and better staffing models, but also some things that have not even been yet thought of.

In addition, I think there are some parts of the modeling that are too pessimistic; but, I understand why they were not included. I will address them below.

On the Pessimistic Side

This study projects through 2029 and the bubble will get a lot bigger in the next 5 to 10 years past that — which will potentially increase the problem. It also assumes a fairly modest $5,000 per year in out-of-pocket medical expenses; it seems almost impossible that number will come close to being accurate.

I would also note that in the near future you will be able to access an interactive tool, where you can make your own assumptions about the future to see how the numbers will vary. For instance, you might believe the out-of-pocket expenses will be $10,000 and you can test that.

The Key Takeaways

You will likely have seen most of these on other sites. I have included some commentary in red.

-

The group being studied is “generally too wealthy to qualify for public means-tested programs, yet not wealthy enough to pay the costs at many seniors housing communities for a sustained period of time.”

-

There are near three-quarters of a million seniors who don’t initially qualify for public assistance, but ultimately “spend down” and end up on Medicaid.

-

Future seniors have lower overall savings and are less likely to have significant pension plan assets.

-

The study projects a “dramatic reduction in the percentage of low-income seniors”. It is possible this might free up governmental resources that might be used by middle-income seniors. But it is possible that these are folks who might not otherwise qualify for Medicaid.

-

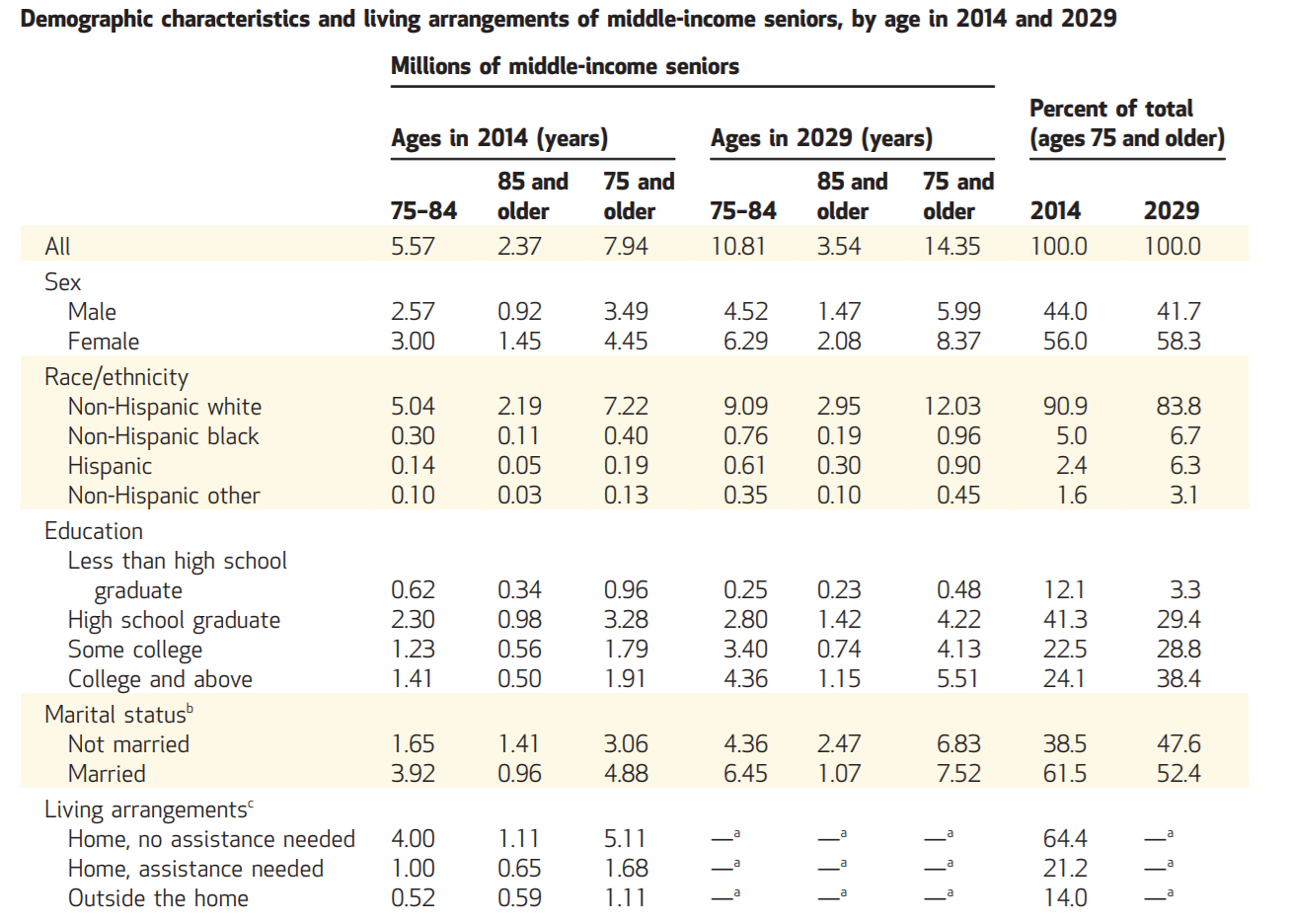

The number of middle-income seniors is expected to double from 7.9 million to 14.4 million.

-

The middle-income group will also account for a larger share of the total number of seniors going from 40% to 43%.

-

The percentage of women and minorities will also increase. It seems likely that the increase in non-white seniors has meaning, though it is unclear what that meaning is, except that we will almost certainly see more minorities taking care of minorities.

-

The senior population is becoming more educated, meaning primarily there are fewer seniors as a percentage who have not gone past high school.

-

Currently, 14% of middle-income seniors (1.11 million) are living in a community setting — assisted living, independent living, or nursing home. This suggests there is some inventory — though right now we don’t have a real quantitative view of what that looks like.

-

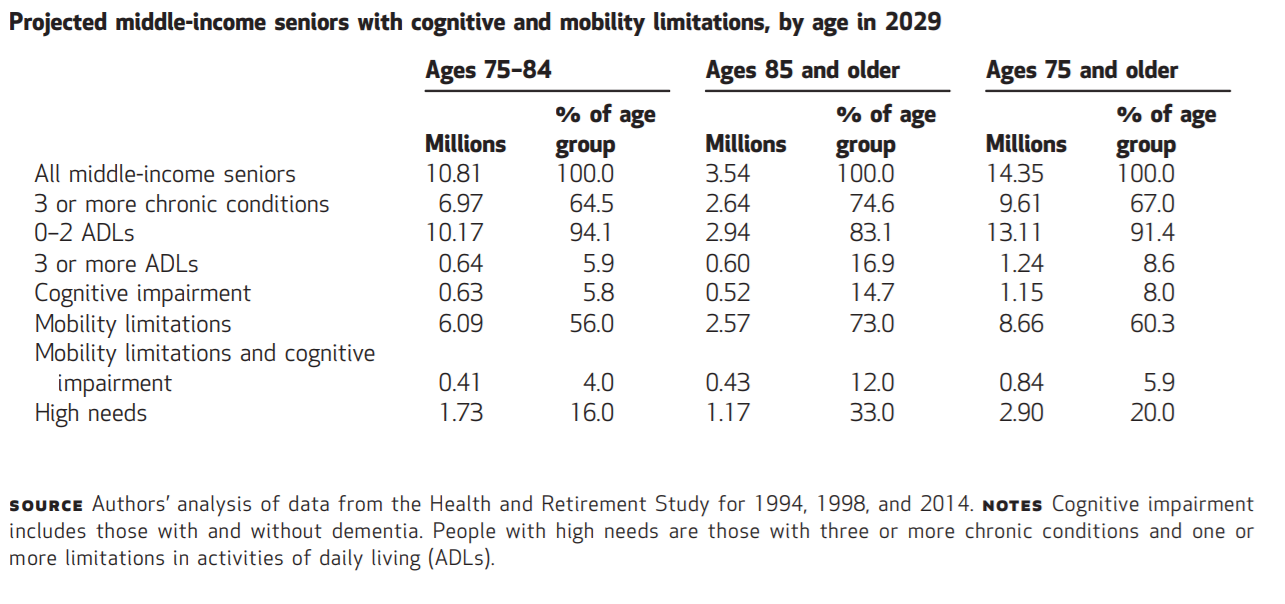

20% of tomorrow’s middle-income seniors will be high need.

-

60% of tomorrow’s middle-income seniors will have mobility limitations.

-

In 2029, 11.6 million middle-income seniors without equity in housing will have an available annual income of $60,000 or less, which is below the projected $62,000 assisted living cost.

-

When you include housing assets, the number improves a bit; however, it still leaves 7.8 million middle-income seniors who are unable to afford senior living.

-

Another way of looking at it is that — if you assume middle-income senior devote 100% of their annual income to senior living — only 19% will be able to afford today’s product. Though when you add in home equity, the number jumps to 46%.

-

Today, approximately 20% of all assisted living residents have some of their care paid for through Medicaid (waiver program).

Solutions from the Study

The study offers a number of potential solutions in two categories: private sector (meaning non-governmental) and public programs. They are all reasonable:

-

A lowered expected investment return. This one seems the least likely to be helpful — though it will ultimately be market-driven, based on other investment options

-

Wealthier residents subsidizing lower-income residents

-

A more basic product for middle market seniors (fewer services and amenities)

-

Technology

-

Improved staff efficiency

-

Encouraging residents to be more self-sufficient

-

Seniors working in the community to earn part of their costs

-

Family caregivers to supplement staff

-

A la carte pricing models

-

Tax incentives for developers and operators

-

Relaxing eligibility requirements for government assistance

-

Subsidies or voucher programs

-

New incentives to encourage better financial planning

-

Senior living organizations establishing Medicare Advantage programs

What’s Missing

As noted earlier, no study can realistically cover everything; however, these seem particularly important when thinking about the problem:

-

We know there is a fair amount of variability with respect to geography and affordability. The study does not attempt to look at geographical differences. This becomes important for a bunch of reasons, not the least of which is that we may very well see more senior migration in order to access more affordable assisted living. Perhaps — in time — even to other countries.

This is a topic that will be discussed at an event that will take place in New York in May. It is also fruitful ground for additional research.

-

The study does not actually address the current and future need in terms of number of units. Meaning something like this: “Based on these numbers, we expect to see a shortfall of X number of thousands of units to meet the need.” According to Beth Mace, you can expect to see some estimates coming out of NIC in the next couple of months.

-

Even today, we don’t have a real sense of what the unmet need is. We do know, as noted earlier, that 14% of middle-income seniors (11 million) are living in a community setting — assisted living, independent living or nursing home. So there is some inventory out there.

-

The study does not account for future inheritances that many Boomers are likely to receive, which will add to their available resources.

-

The study did not really consider that even today — and likely into the future — many families will contribute to the cost of senior living, making up for their parents and grandparents shortfalls.

-

The average length of stay in assisted living today is around 22 months and the study does assume that seniors will spend down in order to qualify. There is not much detail on this in the current document, but it would be a great topic for additional discussion.

-

Because the data is so hard to come by, it does not really factor in residential assisted living, which is significant in some states like California. And while it can be every bit as expensive as traditional senior living, many provide a more modest living arrangement with a more modest cost.

How to Look at All This

I want to be very cautious about you, the reader, seeing this article as criticism of the study . . . specifically because that simply does not reflect my views. This study has huge value to the senior living sector, the healthcare sector, public policy makers, and elected officials. For senior living, it presents a massive and wonderful opportunity to explore the margins of what we do today in order to invent new ways of doing things.

There are two key things we believe . . . I believe anyway . . . about the emerging Boomer population:

-

Most don’t actually want the luxury senior living we are offering today — which is good, because most won’t be able to afford it even if they wanted it. This represents a clean slate to create new and wonderful communities.

-

It is easy to say the Boomers won’t be willing to accept a stripped down version of the luxury 4- to 5-star senior living we are offering today. Yet, when it comes to available resources, I think they will, as long as we are creative about what we are creating. I would point to some of the communities SHAG has created. They are more basic than market rate communities, but very livable.

This is just the beginning of powerful and important conversations.